The High Cost of Copay Accumulators: How Insurers’ Tactics Squeeze Patients and Drugmaker Aid

For 16 years, Larry Gruber, a fitness coach from Wilton Manors, Florida, relied on a crucial coupon card to manage the exorbitant cost of his psoriatic arthritis medication. The drug, Enbrel, manufactured by Amgen, carries a staggering monthly price tag exceeding $7,700. For over a decade and a half, Amgen provided Gruber with a coupon card, a financial lifeline that significantly eased his burden. This card, worth thousands of dollars annually, counted towards his health insurance deductible and out-of-pocket maximum. Typically, by February each year, Gruber would meet his out-of-pocket maximum, allowing his health insurance to cover the remainder of his medical costs and leaving him with zero drug expenses for the rest of the year.

However, this year marked a dramatic and distressing shift in Gruber’s healthcare experience. His new health insurer, Oscar HMO of Florida, decided to withhold the value of the manufacturer’s coupon. Instead of applying it to his cost-sharing obligations, Oscar Health insisted that Gruber pay the full cost of the medication until he personally satisfied the plan’s deductible and out-of-pocket maximum. This change in policy has had a profound financial and emotional impact on Gruber, who had planned to use his accumulated savings for a down payment on a home.

The "Accumulator" Dilemma: Insurers’ Cost-Saving Strategy

Oscar Health’s decision is emblematic of a growing trend among commercial health insurers: the use of "copay accumulator" programs. These programs, also sometimes referred to as copay maximizers or accumulator adjustment programs, are designed to reduce the financial burden on insurers by preventing manufacturer-provided copay assistance from counting towards a patient’s deductible or out-of-pocket maximum. According to Avalere Health, a healthcare consulting firm, an increasing number of insurers have adopted these strategies over the past decade to curb their prescription drug expenditures.

The implications for patients like Larry Gruber are severe. If Oscar Health had applied Amgen’s coupon to Gruber’s cost-sharing, he would have been responsible for approximately $3,000 in covered services. Without this assistance, he was compelled to deplete his personal savings to meet the plan’s substantial $10,600 out-of-pocket maximum.

"The real insult here is that they’re taking the money that’s intended to help you," Gruber stated, his voice laced with frustration and despair. "I feel desperate, pressed against the wall, and squeezed." His dream of homeownership is now in jeopardy, a stark illustration of how these seemingly opaque insurance policies can directly impact patients’ financial stability and life plans.

A Growing National Concern: Data and Scope of the Problem

The use of copay accumulator programs is not an isolated incident. Research indicates a significant and growing prevalence of these practices. A review by The AIDS Institute, a non-profit organization advocating against such programs, found that for the 2026 plan year, nearly 40% of plans available on the Affordable Care Act (ACA) marketplaces incorporate copay accumulator mechanisms. In Florida alone, where Gruber resides, 10 out of the 16 insurers offering plans on the marketplace utilize these programs.

This trend disproportionately affects patients with chronic conditions requiring expensive, often brand-name specialty drugs. Individuals managing autoimmune disorders, multiple sclerosis, diabetes, HIV, and cancer are frequently reliant on manufacturer copay assistance to access life-sustaining or life-improving treatments. Patient advocates argue that delays in treatment or a worsening of these conditions due to affordability issues can ultimately lead to higher overall healthcare costs for both the patient and the healthcare system.

The Competing Narratives: Insurers vs. Drugmakers

The debate surrounding copay accumulator programs is multifaceted, with both insurers and pharmaceutical manufacturers presenting distinct perspectives on their impact.

Matt Choffin, Florida market president for Oscar Health, declined to comment on the specifics of Gruber’s case. However, he articulated the company’s rationale for employing copay accumulators. He stated that these programs are utilized to manage rising medical and prescription drug costs and, crucially, "to keep monthly premiums as low as possible." This argument centers on the idea that by reducing their own expenditure on high-cost drugs, insurers can pass on savings to a broader pool of policyholders through lower premiums.

Conversely, pharmaceutical companies argue that insurers and Pharmacy Benefit Managers (PBMs) employ copay accumulators and similar tactics to obstruct patient access to necessary medications. They contend that these practices can delay or deny care and effectively steer patients towards medications that the insurers or PBMs prefer, often those with more favorable contracts, rather than the most clinically appropriate option for the patient.

A Patient’s Perspective: The Unforeseen Financial Strain

Larry Gruber’s situation highlights the critical importance of his medication. Psoriatic arthritis, a chronic inflammatory disease, can lead to debilitating joint stiffness and pain. For Gruber, who relies on his physical fitness for his livelihood as a trainer, weekly Enbrel injections are essential to prevent his joints from stiffening. He vividly recalls the severity of his diagnosis in 2010, when he struggled with basic tasks like shaking hands or lifting his leg to get into bed. Without consistent treatment, he experiences widespread aches.

Crucially, Enbrel is a biologic medication for which there is no medically equivalent generic alternative. This means Gruber does not have the option of switching to a cheaper drug. His reliance on Enbrel is lifelong, making the financial implications of copay accumulators particularly dire.

Navigating a Complex System: Transparency and Consumer Confusion

A significant challenge for consumers is the lack of transparency surrounding copay accumulator programs. It can be difficult for patients to determine if their health plan utilizes such a program and to understand precisely how it operates. Critics argue that these programs not only render medications unaffordable but also allow insurers to "double-dip" – collecting funds from both the patient (or manufacturer assistance) and potentially from the drugmaker through other channels.

Carl Schmid, executive director of the HIV+Hepatitis Policy Institute, a patient advocacy group, articulates this concern forcefully: "They’re taking the money twice and they’re hurting patients." He questions the logic behind an insurer’s insistence on the source of payment, stating, "Why does it make a difference to Oscar if they get the money from a drug company or, you know, his mother or him? They’re still getting the money."

Regulatory Landscape: State-Level Action and Federal Stalemate

The regulatory environment surrounding copay accumulator programs is complex and fragmented. Medicare and Medicaid programs are prohibited from using these programs due to federal anti-kickback laws, which disallow drug manufacturers from offering financial incentives to influence patient choices. Similarly, the Internal Revenue Service restricts their use with high-deductible health plans paired with health savings accounts. However, individual and commercial group health plans, particularly those sold on the ACA marketplaces, are subject to varying state regulations.

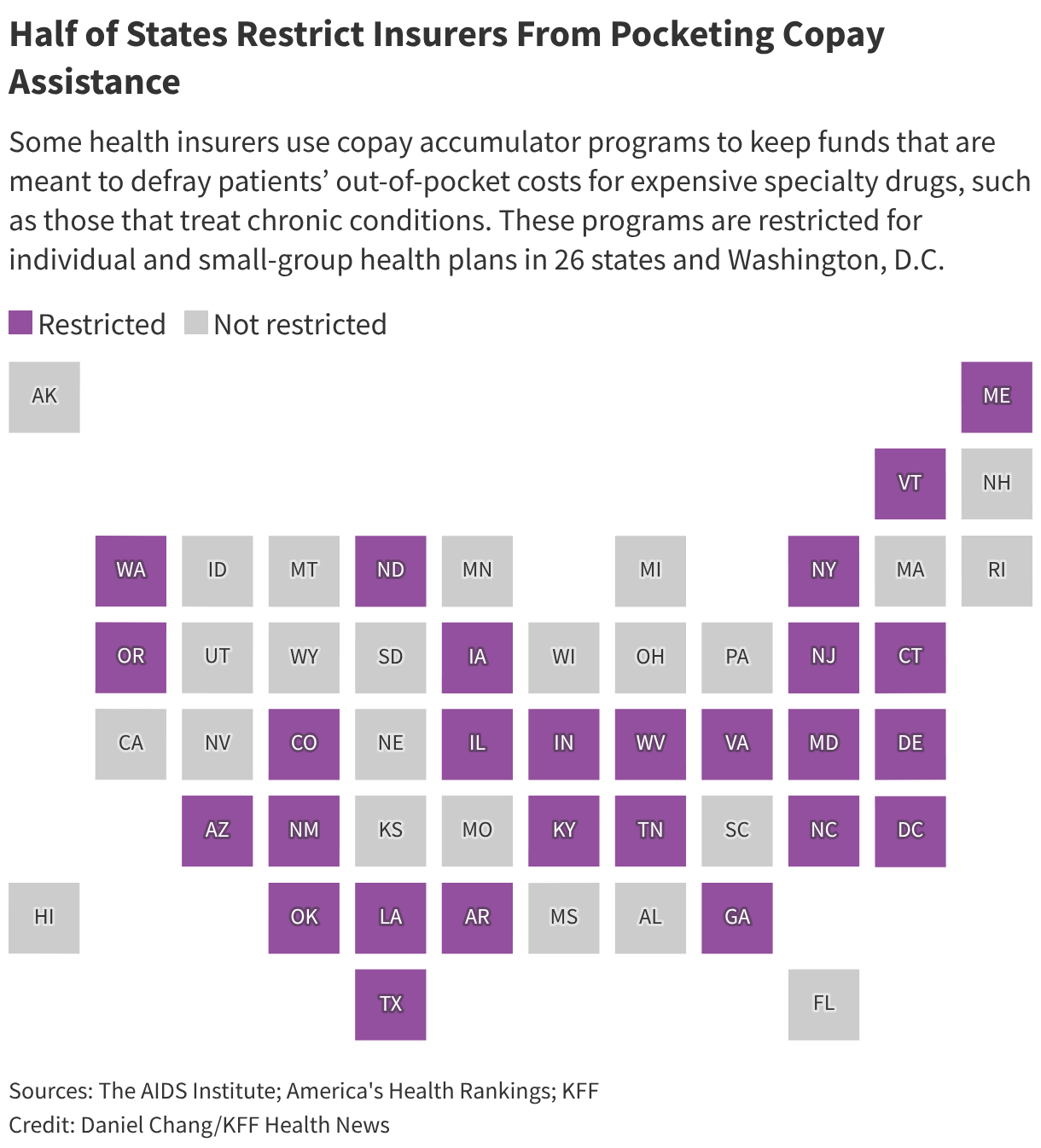

This has led to a patchwork of state laws. Since 2019, an increasing number of states have enacted legislation to ban or restrict copay accumulator programs. Gavin Clingham, public policy director for the Alliance for Patient Access, an advocacy group, notes that 26 states, along with Washington D.C. and Puerto Rico, have adopted laws that either ban copay accumulators entirely or prohibit their use for drugs that lack a generic equivalent. Colorado, for instance, has extended these protections to drugs without a biosimilar. In states without such protections, insurers retain the discretion to implement these programs.

Federal Oversight: A Stalled Effort

Despite growing state-level action, federal regulation of copay accumulator programs remains in a state of flux. A significant development occurred in 2023 when a federal court struck down a Trump-era policy that had permitted insurers to utilize these programs. This ruling led the Department of Health and Human Services (HHS) to revert to an earlier regulation that restricts their use to brand-name drugs that have a medically appropriate generic equivalent.

Following this court decision, the Biden administration had pledged to address copay accumulators through future rulemaking. However, as of the time of reporting, HHS has not yet issued such regulations. This inaction has drawn criticism from patient advocacy groups like the HIV+Hepatitis Policy Institute, which spearheaded a coalition that sued to overturn the previous rule. Schmid emphasizes the potential for federal action, stating, "The Trump administration can stop this once and for all at the national level. If they really care about patient affordability, this is something they can do."

Bipartisan legislative efforts, such as the HELP Copays Act, are aiming to address this gap by requiring financial assistance to count towards deductibles and out-of-pocket costs for federally regulated plans, including many employer-sponsored health benefits. However, this bill has yet to gain significant traction in Congress.

The Consumer’s Predicament: Trapped in the Middle

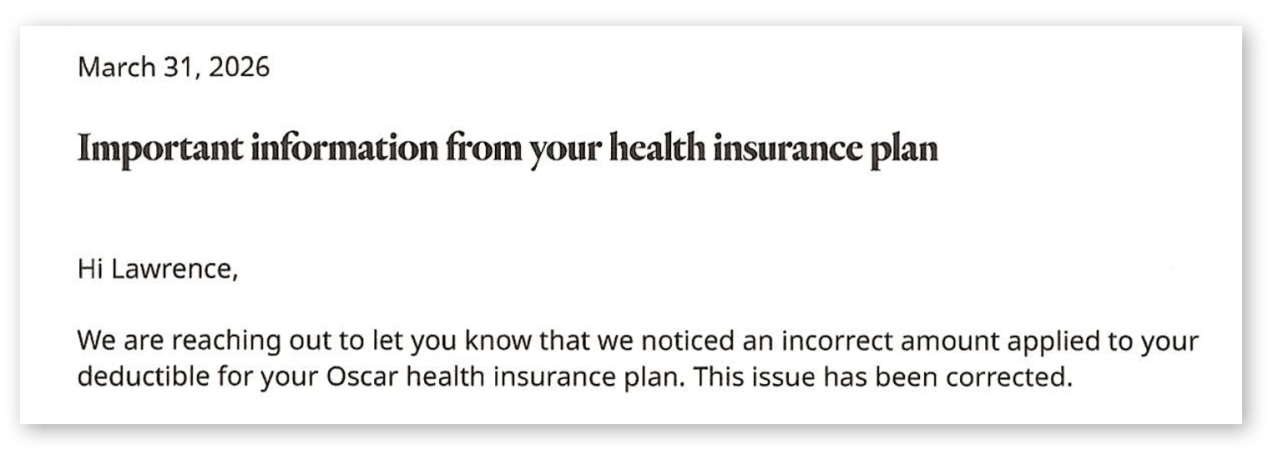

For consumers like Larry Gruber, the current regulatory environment leaves them vulnerable. Gruber’s confusion was compounded when his Oscar Health patient portal initially appeared to be counting his coupon card towards his out-of-pocket maximum. He even believed he had met his maximum by February and that Oscar was covering his medication costs in March. However, when he attempted to refill his prescription in April, the pharmacy informed him that Oscar would only cover a fraction of the cost, leaving him responsible for the remaining $6,700. This was followed by a letter from Oscar Health stating that an "incorrect amount" had been applied to his deductible, a correction that effectively reversed the previous coverage.

"They sent me a letter that basically stated they made a mistake," Gruber recounted, expressing his disbelief. "The fact that they’re allowed to sort of change things midstream is also, I think, a little galling." Faced with this sudden financial burden, Gruber resorted to rationing his injections, taking them every other week instead of weekly, and by May, he was forced to dip into his savings to afford his medication.

Broader Implications and Future Outlook

The widespread adoption of copay accumulator programs raises significant questions about the balance of power between insurers, pharmaceutical manufacturers, and patients. Insurers argue that drugmakers use copay assistance as a tactic to justify exorbitant drug prices and encourage the use of expensive brand-name drugs over potentially more affordable generics. Pharmaceutical companies, conversely, contend that this assistance is vital for patient access and that insurers are exploiting loopholes to increase their profits at the expense of patient well-being.

Patient advocates, such as Rachel Klein, deputy executive director for The AIDS Institute, argue that insurers possess ample tools to manage costs without resorting to copay accumulators. These tools include negotiating drug formularies, determining medical necessity, and requiring patients to try lower-cost alternatives first. "They are the ones making the decisions," Klein asserted. "Now the individual is left trying to figure out how they’re going to pay for it."

For patients like Larry Gruber, the lack of robust federal oversight and the complexities of insurance plans create a precarious situation. Experts advise consumers to meticulously research their health insurance options, carefully review plan documents, and proactively contact their insurance providers or state insurance regulators to inquire about the use of copay accumulator programs before enrollment.

Gruber’s experience serves as a potent reminder of the real-world consequences of these financial strategies. The extra expense has forced him to forgo a vacation this year and jeopardized his savings for a home. The constant worry about affording his essential medication is a daily burden, and he fears that a recurrence of this situation year after year could prove financially devastating. The struggle of individuals like Larry Gruber underscores the urgent need for greater transparency and more comprehensive regulatory action to ensure that financial assistance intended to help patients ultimately reaches those who need it most.

{kind=link}