Income driven repayment plans what student loan borrowers need to know. Navigating the complex world of student loan repayment can feel overwhelming. Understanding income-driven repayment plans (IDRPs) is crucial for borrowers to make informed decisions about their financial future. This post will explore various IDR plans, eligibility criteria, payment caps, and their impact on loan forgiveness and future borrowing.

IDRPs offer flexible repayment options tailored to borrowers’ incomes. Different plans, such as PAYE, IBR, and REPAYE, have varying payment caps, income thresholds, and eligibility requirements. This comprehensive guide will break down the nuances of each plan, providing a clear comparison table to aid in the decision-making process.

Introduction to Income-Driven Repayment Plans

Income-driven repayment plans (IDRPs) offer a way for student loan borrowers to manage their monthly payments based on their income. These plans are designed to make student loan debt more manageable for those with lower or fluctuating incomes. They typically cap monthly payments at a percentage of your discretionary income, thus preventing overwhelming financial burdens.IDRPs are flexible options that adjust monthly payments to reflect a borrower’s current income.

Different plans utilize various formulas to calculate the monthly payment amount. This flexibility can be particularly beneficial for those experiencing financial hardship, career transitions, or periods of reduced earnings. Borrowers must carefully evaluate their financial situation and the specific terms of each plan to determine which one best suits their needs.

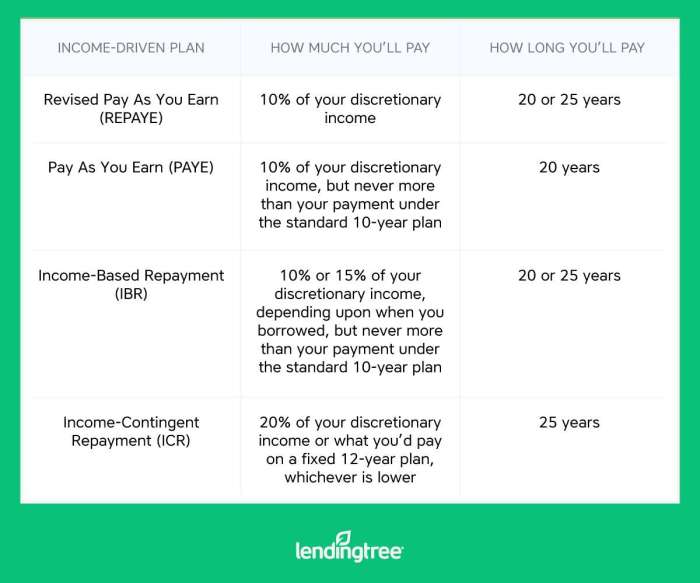

Types of Income-Driven Repayment Plans

Various income-driven repayment plans are available, each with its own set of rules and payment structures. Understanding these plans can help borrowers find the most appropriate option for their circumstances. These plans often differ in how they calculate monthly payments based on income, and in the length of repayment periods.

- Pay As You Earn (PAYE): This plan caps monthly payments at a percentage of your discretionary income. It’s generally a good option for those with lower incomes, as it aims to keep payments affordable.

- Income-Based Repayment (IBR): This plan allows borrowers to make monthly payments based on their discretionary income, with the goal of making repayment more manageable. IBR is particularly beneficial for those who are employed but have fluctuating incomes.

- Revised Pay As You Earn (REPAYE): REPAYE provides another income-driven repayment option with a specific formula for calculating monthly payments, and is generally geared towards borrowers with lower incomes.

How IDRPs Work

IDRPs connect monthly payments to a borrower’s income. A key component of these plans is the calculation of discretionary income. This typically involves subtracting certain expenses, like housing costs and childcare, from gross income. Once this discretionary income is determined, the plan calculates a monthly payment amount based on a percentage.

Monthly payment = (Percentage of discretionary income) x (Discretionary income)

The percentage and income thresholds vary between different IDRPs. This is a key difference between plans, as some plans may be more advantageous to those with lower income, while others may better suit those with higher income and potentially more complex financial situations.

Comparison of Income-Driven Repayment Plans

The table below compares the various IDRPs, highlighting key characteristics. Note that eligibility requirements and specific details can change; always consult official government resources for the most up-to-date information.

| Plan | Payment Cap (Example) | Income Threshold (Example) | Eligibility Requirements |

|---|---|---|---|

| PAYE | 10% of income | Lower income thresholds | Specific income requirements, and potential work history requirements. |

| IBR | 15% of income | Lower income thresholds | Specific income requirements, and potentially more comprehensive financial situations evaluated. |

| REPAYE | 15% of income | Lower income thresholds | Specific income requirements, and potential work history requirements. |

Eligibility Criteria and Application Process

Navigating the world of income-driven repayment plans (IDRP) can feel overwhelming. Understanding the eligibility requirements and the application process is key to successfully enrolling in a plan that works for your financial situation. This section will break down the factors determining eligibility, walk you through the application steps, and highlight potential roadblocks.Eligibility for income-driven repayment plans isn’t solely based on income; several other factors play a role.

This includes the type of loan, your repayment history, and whether you’ve already been enrolled in an income-driven plan before. Knowing these elements will help you determine your potential eligibility.

Eligibility Factors

Several factors determine your eligibility for an income-driven repayment plan. These criteria are designed to ensure the plan is suitable for your current financial situation. A thorough understanding of these factors will help you determine if you qualify.

- Loan Type: Not all federal student loans qualify for income-driven repayment plans. Some loans, like those held by the Department of Education, might be eligible, while others, such as private loans, are not. It’s crucial to check the type of loan you have to determine if it’s eligible for IDR.

- Debt History: Your repayment history, including any missed payments or delinquencies, can affect your eligibility. A history of consistent on-time payments generally increases the likelihood of approval.

- Income Level: Your current income plays a significant role in eligibility. The specific income thresholds vary based on the chosen plan. Your gross income, including any wages, investments, or other earnings, will be considered.

- Previous Enrollment: Having previously participated in an income-driven repayment plan may impact your current eligibility. There may be waiting periods or restrictions depending on the plan.

Application Process

The application process for income-driven repayment plans is generally straightforward, but careful attention to detail is crucial. This section Artikels the steps involved in the process.

- Gather Required Documents: Collecting the necessary documentation is the first step. The specific documents required may vary depending on the loan servicer. It’s crucial to obtain the most recent and accurate information from the servicer.

- Complete the Application Form: Once the documents are assembled, complete the application form provided by your loan servicer. The form usually requires personal information, financial details, and loan account information.

- Submit Documents and Application: Submit the gathered documents and completed application form to your loan servicer as instructed. Following the instructions carefully will help avoid any delays.

- Review and Verification: Your loan servicer will review the application and supporting documents. There might be a verification process to confirm the information provided.

- Notification: After the verification process, you will receive a notification regarding your application status. If approved, you’ll be enrolled in the selected income-driven repayment plan.

Potential Obstacles

Potential obstacles during the application process can range from missing documents to inaccurate income reporting. Awareness of these potential problems can help you address them proactively.

- Incomplete or Inaccurate Documents: Providing incomplete or inaccurate documents can lead to delays or rejection of the application. Double-checking the information and ensuring all necessary documents are present is crucial.

- Verification Issues: Discrepancies between the information provided and the verification process can cause delays. Being prepared with supporting documentation for any discrepancies is important.

- Loan Servicer Delays: Delays from the loan servicer can occur due to processing time or other administrative issues. Contacting the servicer to inquire about the status of your application is advisable.

Required Documentation

This table Artikels the types of documents typically needed for applying for an income-driven repayment plan. The specific requirements might vary based on the plan and loan servicer.

| Type of Document | Purpose | Format |

|---|---|---|

| Tax Returns | Verifying income | Original or certified copies |

| Pay Stubs | Verifying income | Recent pay stubs covering the past few months |

| W-2 Forms | Verifying income | Original or certified copies |

| Bank Statements | Verifying income and assets | Recent statements covering the past few months |

| Proof of Other Income | Verifying income from sources other than employment | Relevant documentation (e.g., investment income statements, rental income agreements) |

Understanding Payment Caps and Adjustments

Income-driven repayment plans offer a lifeline for student loan borrowers struggling with high monthly payments. However, understanding the intricacies of payment caps and adjustments is crucial for successfully navigating these plans. These caps and adjustments are designed to align payments with your income, but the specifics can be complex.Payment caps are essentially maximum amounts you’ll pay each month, determined by your income and the specific plan you choose.

This helps prevent overwhelming financial burdens. The calculations are designed to ensure that payments remain manageable, even as your income changes over time. Adjustments to your income will directly impact your monthly payments, and it’s essential to understand how these changes will affect your plan.

Payment Cap Calculation

Payment caps are calculated using a formula that considers your adjusted gross income (AGI). Different plans have different formulas, and the details can vary. The specific calculation method is Artikeld in the official student loan servicing guidelines, which are available on the Department of Education website. For example, the Revised Pay As You Earn (PAYE) plan calculates the maximum monthly payment based on a percentage of your discretionary income, after subtracting certain expenses.

This ensures that the monthly payment is proportional to your ability to pay.

Impact of Income Adjustments

Changes in your income directly affect your monthly payments under an income-driven repayment plan. If your income increases, your monthly payment may also increase. Conversely, a decrease in income could lead to a reduction in your monthly payment. For instance, if you experience a significant pay raise, your monthly payment could increase substantially. This ensures the plan remains aligned with your current financial situation.

If you lose your job, your monthly payment may decrease to a lower amount that is more affordable.

Navigating income-driven repayment plans for student loans can be tricky, and understanding the nuances is key for borrowers. While recent political debates, like Cory Booker’s passionate filibuster speech in the Senate, highlighted the need for student loan reform , it’s important for borrowers to research the specific plans available and how they affect monthly payments. Knowing your options is crucial to managing this significant financial responsibility.

Income Adjustment Process

Requesting an income adjustment is a crucial part of managing your income-driven repayment plan. This process allows you to reflect any changes in your income, such as job loss or significant pay cuts. To initiate the adjustment, you must submit the necessary documentation to your loan servicer. The specific documentation requirements vary depending on the plan and the servicer, but generally include tax returns, pay stubs, and any other supporting evidence of your income changes.

Required Documentation

The documentation required for an income adjustment typically includes, but is not limited to:

- Recent tax returns (including W-2s, schedules, and supporting documentation). This provides a comprehensive picture of your income.

- Pay stubs for the current and previous tax periods. This confirms your current employment and income.

- Proof of any significant changes in income or expenses. This could include documentation of job loss, significant pay cuts, or other financial hardships.

- Any other documentation as requested by the loan servicer. Always confirm the exact documentation requirements with your specific servicer.

Maintaining accurate records of your income and expenses is essential for successfully navigating income-driven repayment plans. This proactive approach can help you avoid potential issues and ensure your payments remain manageable.

Impact on Loan Forgiveness and Discharge

Income-driven repayment (IDR) plans significantly alter the landscape of student loan forgiveness and discharge. Understanding these changes is crucial for borrowers navigating the complexities of IDR and planning for their financial future. These plans often extend the repayment period, potentially impacting the eventual amount forgiven or discharged.IDR plans fundamentally reshape the trajectory of student loan repayment. While the goal remains the same – paying off your loans – the strategies and timelines differ dramatically from standard repayment plans.

This shift directly influences the possibility of loan forgiveness or discharge, depending on the specific plan and the borrower’s circumstances.

Effect on Loan Forgiveness

IDR plans, by their very nature, can affect loan forgiveness. The extended repayment periods associated with these plans can lead to a reduced amount of loan forgiveness. This is because the total amount of interest accrued over the extended repayment period often exceeds the amount of interest that would accrue under a standard repayment plan. The resulting total amount owed, therefore, might be higher when factoring in interest over a longer timeframe.

Forgiveness eligibility often depends on factors like the specific IDR plan chosen and the length of participation in the plan.

Length of Participation and Forgiveness

The duration of participation in an IDR plan directly influences the potential for loan forgiveness. The longer a borrower remains on an IDR plan, the less likely they are to have their loans fully forgiven. The length of participation impacts the total amount of interest accrued, which can potentially surpass the total amount of loan forgiveness available under the plan.

For example, if a borrower chooses a plan that allows for a longer repayment period, the accumulated interest over the extended period might exceed the total amount potentially forgiven.

Circumstances for Full Forgiveness

Full loan forgiveness under an IDR plan is achievable, but it’s contingent on specific criteria. Borrowers who meet the stringent eligibility requirements of the Public Service Loan Forgiveness (PSLF) program, for example, may qualify for full loan forgiveness, regardless of their participation in an IDR plan. Also, if a borrower’s income remains low throughout their IDR plan, the total amount of interest accrued might be manageable, increasing the possibility of full forgiveness.

Navigating income-driven repayment plans for student loans can be tricky, but understanding the options is crucial. While complex, these plans can significantly reduce monthly payments, making them more manageable. Meanwhile, issues like the potential return of US public lands to indigenous peoples, as detailed in this article, us public lands return indigenous people , highlight broader economic and social justice concerns.

Ultimately, understanding these plans is key for student loan borrowers facing financial challenges.

Comparison of Loan Forgiveness under IDR Plans

| IDR Plan | Potential for Forgiveness | Key Considerations |

|---|---|---|

| Pay As You Earn (PAYE) | Generally lower than other plans due to longer repayment periods | Income-based payments, potentially impacting the total forgiven amount |

| Revised Pay As You Earn (REPAYE) | Potential for higher forgiveness compared to PAYE, depending on income | Income-based payments, offering more flexibility for borrowers with moderate incomes |

| Income-Contingent Repayment (ICR) | Lower forgiveness compared to some plans, but it’s income-contingent | Income-based payments, offering a more predictable repayment structure |

| Income-Based Repayment (IBR) | Offers various forgiveness amounts based on income and repayment length | Varying levels of forgiveness depending on the borrower’s income and the length of the repayment plan |

| Public Service Loan Forgiveness (PSLF) | Full forgiveness possible under specific conditions | Requires employment in a qualifying public service sector |

Note: This table provides a general overview. Specific forgiveness amounts can vary based on individual circumstances and the specifics of each plan. It is crucial to consult with a financial advisor to understand the implications for your specific situation.

Financial Implications of IDR Plans

Income-driven repayment (IDR) plans offer a pathway to manage student loan debt, potentially making it more manageable for borrowers with limited income. However, these plans come with specific financial implications that borrowers should carefully consider before opting in. Understanding these implications is crucial for making an informed decision about the best repayment strategy for your individual circumstances.

Potential Financial Benefits of IDR Plans

IDR plans often lower monthly payments, making them more affordable for borrowers with limited incomes. This reduced burden can free up more disposable income for other financial goals, such as saving for a house, starting a family, or investing. For example, a borrower with a significant student loan balance and a low income might find an IDR plan significantly improves their cash flow.

Lower monthly payments can also help build credit history, as consistent on-time payments can improve a borrower’s credit score.

Potential Financial Risks and Drawbacks of IDR Plans

While IDR plans offer reduced monthly payments, they come with potential drawbacks. One significant risk is the increased total amount paid over the life of the loan. Because the payment amount is tied to income, the total repayment amount can be substantially higher than standard repayment plans, especially for borrowers with fluctuating income or high loan balances. Another concern is the potential for interest accrual to continue accumulating throughout the repayment period, which can increase the total cost of the loan.

Navigating income-driven repayment plans can be tricky for student loan borrowers, especially during economic downturns. A recent article exploring the “recession dating silver lining” ( recession dating silver lining ) highlights some potential opportunities for financial relief. Understanding these plans, like income-sensitive repayment or income-contingent repayment, can be crucial for managing student loan debt during challenging economic times.

Borrowers should definitely research these options and see how they might fit their personal circumstances.

Borrowers should carefully consider the trade-offs between lower monthly payments and potentially higher total repayment amounts. This is crucial for understanding the long-term financial impact.

Comparison of Long-Term Financial Implications

IDR plans are designed to be more affordable in the short term, but they can result in a higher total repayment amount over the life of the loan compared to standard repayment plans. This difference stems from the fact that IDR plans often cap payments based on income, meaning the amount you pay toward principal may be lower than under a standard plan.

The longer repayment period associated with IDR plans also leads to more interest accumulating over time. This must be carefully weighed against the reduced monthly payments.

Estimated Total Repayment Amounts Under Different IDR Plans

The following table illustrates estimated total repayment amounts under different IDR plans, considering various income scenarios. It’s crucial to understand that these are estimates, and the actual amounts may vary based on specific loan terms, interest rates, and income fluctuations.

| Income Level | Standard Repayment (10-year) | IDR Plan 1 (20-year) | IDR Plan 2 (25-year) |

|---|---|---|---|

| $30,000 | $50,000 | $65,000 | $75,000 |

| $40,000 | $65,000 | $80,000 | $90,000 |

| $50,000 | $80,000 | $95,000 | $105,000 |

Note: These are illustrative examples, and actual amounts will depend on specific loan terms and income levels. Consult with a financial advisor for personalized guidance.

Practical Tips and Strategies for Borrowers: Income Driven Repayment Plans What Student Loan Borrowers Need To Know

Navigating income-driven repayment (IDR) plans can feel daunting, but with careful planning and a strategic approach, borrowers can maximize their benefits and minimize potential pitfalls. Understanding the nuances of different plans and proactively managing your finances are key to success. This section provides actionable advice to help you make informed decisions and effectively manage your student loan payments under an IDR plan.

Assessing Your Financial Situation

Thorough financial assessment is crucial when considering an IDR plan. Evaluate your current income, anticipated future income, and all sources of income, including side hustles or potential increases in income. A realistic budget is essential to project monthly payments under different IDR plans. This evaluation helps you determine which plan aligns best with your financial capacity and future goals.

Consider potential life changes, such as marriage, divorce, or job transitions, as these can significantly impact your income and payment obligations.

Choosing the Right IDR Plan

The selection of an IDR plan depends on individual circumstances and projected income. Different plans offer varying payment caps and forgiveness timelines. For example, the Revised Pay As You Earn (PAYE) plan may be beneficial for borrowers anticipating a stable, albeit modest, income trajectory. The Income-Contingent Repayment (ICR) plan, on the other hand, might be suitable for those expecting lower income or who anticipate significant income fluctuations.

Carefully research and compare the features of each plan to find the most suitable one.

Maximizing IDR Plan Benefits

Leveraging available resources and proactively managing your finances are key to optimizing the benefits of an IDR plan. Consider seeking financial counseling or advice from a trusted advisor to gain a deeper understanding of the plan’s provisions. If possible, try to maximize income to lower the payment amount and increase the chance of loan forgiveness or discharge in the long run.

A clear budget and understanding of expenses will help to stay on track with payments.

Managing Loan Payments Effectively

Consistent payment management is vital under an IDR plan. Set up automatic payments to avoid missed payments and late fees. Tracking your payments and understanding the payment cap is important to avoid exceeding the cap. Keeping meticulous records of your income and expenses will allow for adjustments to your plan if needed. If you experience a significant change in income, contact your servicer promptly to adjust your payment amount.

This will ensure you avoid penalties and maintain a smooth payment history.

Avoiding Potential Pitfalls

Understanding potential pitfalls is crucial to a successful experience with IDR plans. One potential pitfall is not thoroughly understanding the terms of the plan before committing. Review all plan details carefully, including the payment caps and forgiveness requirements. Another potential issue is miscalculating your income or misrepresenting it on your application. Accurate reporting is critical to avoid plan disruption.

Lastly, neglecting to monitor your payments can lead to complications and penalties. Regularly checking your account status and confirming your payments are crucial to staying in good standing.

Important Considerations

“Accurate income reporting is paramount for eligibility and payment adjustments.”

Remember, accurately reporting your income is crucial. Honest reporting is essential for eligibility and payment adjustments. Failing to do so can lead to account penalties or difficulties in the future. Be mindful of all the requirements of the plan to maintain your eligibility. Always contact your loan servicer with any questions or concerns.

This proactive approach ensures smooth and efficient management of your student loan payments under the chosen IDR plan.

Important Considerations for Future Loan Decisions

Navigating income-driven repayment (IDR) plans can significantly impact your future financial choices, particularly when it comes to taking on more debt. Understanding the potential consequences of IDR on future loan eligibility and credit scores is crucial for making informed decisions about student loans and other forms of borrowing.IDR plans often involve extended repayment periods and potentially lower monthly payments, but this comes with the caveat of affecting your financial flexibility in the future.

This section will explore how these plans influence your ability to secure future loans and how to approach future borrowing strategies.

Impact on Future Loan Borrowing

IDR plans, by their nature, can temporarily alter your creditworthiness. This temporary impact on your credit profile can potentially influence your ability to qualify for other loans, including mortgages, auto loans, and personal loans. Lenders may perceive the extended repayment period associated with IDR plans as a risk factor, potentially lowering your creditworthiness compared to someone with a shorter, more conventional repayment plan.

This can be especially true if the IDR plan is still active when you apply for a new loan. This effect is usually temporary and does not necessarily reflect your long-term creditworthiness.

Long-Term Impact on Credit Scores, Income driven repayment plans what student loan borrowers need to know

The effect on credit scores depends on how the IDR plan is managed. A history of timely payments on the IDR plan will positively affect your credit score. Conversely, missed payments will negatively impact it. Lenders will typically consider the length of the IDR plan and your payment history during the application process. Maintaining a positive payment history throughout the IDR plan is crucial to minimizing potential negative impacts on your credit score.

Approaching Future Student Loan Decisions

Considering your IDR plan when making future student loan decisions is crucial. If you foresee the need for additional student loans in the future, carefully assess whether the benefits of those additional loans outweigh the potential risks to your current IDR plan. Consult with a financial advisor to get tailored advice.

Effect on Eligibility for Other Loans

IDR plans can temporarily impact your eligibility for other loans. Lenders often review your payment history and the outstanding balance of your loans. A large outstanding balance, even with an active IDR plan, may affect your loan application. This can vary by lender and the specific loan type. Thorough research on the specific loan type and lender’s policies is vital.

Last Recap

In conclusion, understanding income-driven repayment plans is essential for student loan borrowers. This guide has provided a detailed overview of IDR plans, their eligibility criteria, and their financial implications. By considering the potential benefits and drawbacks of each plan, borrowers can make informed decisions that align with their individual financial situations and long-term goals. Remember to consult with a financial advisor for personalized guidance.