How to talk about money with partner is a crucial conversation for any relationship. It’s not always easy, but open and honest communication about finances builds trust and strengthens your bond. This guide provides a roadmap to navigate the often-tricky terrain of financial discussions with your partner, ensuring a comfortable and productive dialogue. From setting the stage for open communication to managing disagreements and maintaining ongoing financial health, we’ll explore all the critical aspects of this essential topic.

This comprehensive guide will cover essential steps to ensure your financial discussions are productive, respectful, and ultimately beneficial to your relationship. We’ll explore how to create a safe space for these talks, understand each other’s financial situations, and establish shared financial goals. Ultimately, we’ll equip you with strategies for managing debt, savings, investments, and navigating any disagreements that may arise.

Setting the Stage for Open Communication

Honest and open communication about money is crucial for a healthy and lasting relationship. Financial discussions can be challenging, but navigating them together strengthens your bond and allows for informed decisions about your shared future. Addressing financial matters proactively prevents misunderstandings and resentment from building.Open dialogue about finances isn’t just about the numbers; it’s about fostering trust, respect, and shared goals.

This foundation paves the way for making sound financial choices as a couple and achieving your aspirations together.

Importance of Discussing Finances

Financial transparency fosters trust and strengthens the relationship. Open communication about financial situations allows for a deeper understanding of each partner’s financial background, goals, and concerns. This understanding is vital in creating a shared financial plan and avoiding potential conflicts.

Creating a Safe and Comfortable Environment

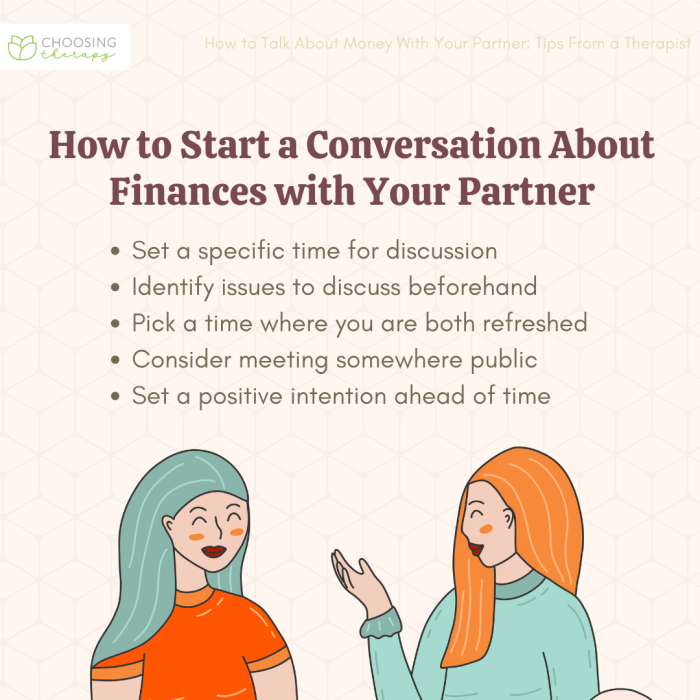

Establishing a safe space for financial discussions is paramount. Choose a time and place where you both feel relaxed and comfortable expressing your thoughts and feelings without pressure or judgment. Avoid discussing money when stressed, tired, or rushed. A calm and supportive atmosphere encourages open dialogue.

Initiating a Conversation

Initiating a conversation about money can feel daunting. Start with a simple, open-ended question about each other’s financial experiences. For example, “What are your thoughts on our current spending habits?” or “What are your long-term financial goals?” Active listening and empathy are key to fostering a receptive environment.

Addressing Discomfort or Resistance, How to talk about money with partner

Discomfort or resistance during financial discussions is normal. Acknowledge these feelings without judgment. Emphasize that the goal is understanding each other’s perspectives and finding solutions together. Focus on finding common ground and shared values, and validate each other’s feelings. A gentle approach that prioritizes empathy can effectively navigate these hurdles.

Establishing Mutual Respect and Understanding

Mutual respect and understanding are essential for successful financial discussions. Actively listen to each other’s perspectives, validate their feelings, and avoid making assumptions. Remember that financial experiences and backgrounds differ, and respect for these differences is crucial. Demonstrate a willingness to compromise and find solutions that benefit both partners.

Financial Discussion Topics

A structured approach to financial discussions ensures that all important aspects are covered. Consider these topics:

- Budgeting: Developing a joint budget helps you track income, expenses, and savings. Understanding your shared financial picture allows for informed decisions and helps you both achieve your financial goals.

- Saving: Establishing a savings plan together is essential for achieving both short-term and long-term financial goals. A joint savings plan fosters a sense of shared responsibility and encourages financial stability.

- Debt: Addressing existing debts, such as student loans or credit card debt, is important for managing your financial health. A proactive approach to debt management allows for the creation of a plan to reduce debt and build financial security.

- Spending Habits: Understanding each other’s spending habits helps identify areas where you can potentially save or adjust your spending patterns. This understanding fosters transparency and enables you to make more informed decisions together.

- Financial Goals: Discussing long-term financial goals, such as purchasing a home, starting a family, or retiring comfortably, is essential. Shared goals provide motivation and direction for your financial decisions.

Understanding Each Other’s Financial Situations

Opening up about finances with a partner can feel daunting, but it’s a crucial step toward a shared financial future. Transparency and understanding are key. This stage requires a willingness to be vulnerable and to listen without judgment. It’s about building trust and a foundation of mutual respect, acknowledging that each person’s financial journey is unique.Understanding individual financial histories is essential for a healthy financial partnership.

Open communication about finances is key in any relationship, especially when discussing shared resources. Navigating those conversations can be tricky, but it’s essential. For example, a complex issue like the recent Texas bill restricting abortion access highlights the importance of understanding each other’s values and beliefs, which often impacts financial decisions. Texas bill abortion ban is a prime example of how societal issues influence personal finances and shared values, further emphasizing the need for open communication with your partner about money.

Ultimately, honesty and understanding are vital when discussing money matters.

This isn’t about assigning blame or dwelling on past mistakes, but rather about learning from the past to build a more secure future together. Each person’s experiences shape their current financial situation, influencing their perspectives, attitudes, and approaches to money management. These insights allow for empathy and informed decision-making as a couple.

The Significance of Individual Financial Histories

A person’s financial history offers valuable insights into their values, habits, and approaches to money. For instance, someone who grew up in a financially secure household might have a different perspective on saving and investing than someone who experienced financial hardship. Understanding these differing backgrounds is vital for a successful financial partnership. These differences in experience don’t need to be seen as negative; rather, they provide opportunities for learning and compromise.

Examples of Discussing Past Financial Experiences

When discussing past financial experiences, focus on the lessons learned and how those experiences have shaped current financial decisions. Avoid dwelling on mistakes or making comparisons that might lead to negativity or resentment. Instead, focus on constructive conversations about what worked well, what didn’t, and how those experiences have led to the present financial situation. For example, “I struggled with impulse purchases in the past, so I’ve since adopted a budgeting app to help me track my spending.” This approach fosters understanding and mutual support, not judgment.

Comparing and Contrasting Different Financial Situations

Differences in income, debt levels, and savings are common in partnerships. It’s crucial to acknowledge these differences and discuss how they will impact joint financial decisions. For example, if one partner has significantly higher income, they might be able to contribute more to savings or debt repayment. Conversely, if one partner has substantial debt, understanding the timeline for repayment is essential for joint budgeting.

Talking openly about money with your partner can be tricky, but it’s crucial for a healthy relationship. It’s all about establishing clear communication and financial goals. News this week about the prisoner swap involving US-Russian dual national Ksenia Karelina, released from Moscow here , highlights the importance of diplomacy and negotiation in complex situations, which can be surprisingly similar to how you navigate financial conversations with your partner.

Ultimately, honesty and proactive discussion are key to a harmonious financial future together.

The goal is not to erase the differences but to understand how they affect shared financial goals.

Common Financial Anxieties and Fears

Financial anxieties are common, and recognizing them is the first step to addressing them. Some common fears include the fear of not having enough money, the fear of making mistakes, and the fear of not being able to provide for loved ones. Acknowledging these anxieties and creating a safe space to discuss them can help build trust and foster a supportive environment.

For example, “I’ve always been worried about unexpected expenses, so we should set aside a contingency fund.”

The Value of Active Listening and Empathy

Active listening and empathy are crucial during these conversations. Listen attentively to your partner’s perspective, validate their feelings, and try to understand their financial motivations. Avoid interrupting or offering unsolicited advice. Empathy allows you to understand their anxieties and concerns, promoting understanding and a shared vision for the future. Empathy also helps create a space where both partners feel heard and valued.

Questions to Ask About Each Other’s Financial Situations

| Category | Questions to Ask |

|---|---|

| Income and Expenses | What are your current income sources and monthly expenses? How have they changed over time? |

| Savings and Investments | What are your current savings goals? How much have you saved in the past? Do you have any investment accounts? What is your investment strategy? |

| Debt | What are your current debts (e.g., student loans, credit card debt)? What are your plans for managing or reducing these debts? |

| Financial Goals | What are your short-term and long-term financial goals? How do you plan to achieve them? |

| Financial Values and Habits | What are your core financial values (e.g., frugality, generosity)? What are your financial habits and routines? |

Establishing Shared Financial Goals: How To Talk About Money With Partner

Having open conversations about money is a crucial step in a healthy relationship, but it’s equally important to work together to achieve shared financial objectives. These shared goals provide a roadmap for your future, fostering a sense of unity and purpose in managing your finances. Defining and prioritizing these goals allows you to effectively allocate resources, leading to greater financial stability and a more satisfying financial life together.Shared financial goals act as a compass, guiding your financial decisions and ensuring you’re both working towards the same objectives.

This alignment promotes mutual understanding and respect, creating a stronger foundation for your relationship. It’s about building a future together, not just individually.

Open communication about finances is key in any relationship. Talking about money with your partner can be tricky, but it’s crucial for a healthy partnership. Learning about financial responsibility is similar to learning about the fascinating world of reptiles, like those featured in earth day snakes lessons. Both require careful consideration and understanding to avoid misunderstandings.

Ultimately, honest conversations are essential for a strong and secure financial future together.

Benefits of Establishing Shared Financial Goals

Shared financial goals are not just about saving for a house; they encompass a broader range of objectives. Establishing shared financial goals offers several significant advantages:

- Improved communication and understanding: When you discuss and define your financial aspirations, it fosters deeper communication and a more comprehensive understanding of each other’s financial perspectives and priorities. This can lead to greater empathy and support.

- Enhanced financial stability: Working towards shared goals often leads to better financial planning and decision-making, increasing financial stability and security for both partners.

- Increased motivation and commitment: Having common objectives strengthens the commitment and motivation to achieve them, fostering a shared sense of responsibility and progress.

- Stronger relationship foundation: Collaborating on financial goals creates a shared sense of purpose and builds a stronger foundation for the relationship, fostering a sense of unity and mutual support.

Types of Shared Financial Goals

Defining shared financial goals can include a variety of objectives. Here are some examples:

- Saving for a down payment on a house: This is a common long-term goal, often requiring significant savings over several years. Careful budgeting and potentially seeking financial advice can make this goal achievable.

- Paying off high-interest debt: Consolidating and paying off debts, such as credit card balances or personal loans, is often a priority. Creating a debt reduction plan and sticking to it is essential for achieving this goal.

- Saving for a significant purchase: Whether it’s a car, a vacation, or a major appliance, setting a savings target and sticking to a budget can make this goal a reality.

- Building an emergency fund: Having a financial safety net is crucial for unexpected expenses. Regular contributions to an emergency fund can provide peace of mind and protect you from financial hardship.

- Planning for retirement: Retirement planning should be considered early in life. Contributing to retirement accounts and understanding investment strategies can set you up for a secure retirement.

Creating a Joint Financial Plan

Creating a joint financial plan is a collaborative process. It’s about working together to define your financial objectives and strategies. Here’s how to approach it:

- List all financial goals: Write down all financial goals, big or small, that you and your partner share. This is the starting point for your plan.

- Assign values and priorities: Determine the importance and urgency of each goal. This will help you prioritize and allocate resources effectively.

- Set realistic timelines: Break down each goal into smaller, manageable steps with specific deadlines. Realistic timelines are crucial for maintaining motivation and tracking progress.

- Establish a budget: Create a joint budget that aligns with your goals and allows you to allocate resources effectively towards achieving them.

- Regular review and adjustments: Schedule regular meetings to review your progress and make adjustments to your plan as needed.

Prioritizing Goals and Creating a Timeline

Prioritizing goals involves understanding the urgency and importance of each objective. For example, paying off high-interest debt may be prioritized over saving for a vacation, as it can save you money in the long run.Creating a timeline involves breaking down each goal into smaller, manageable steps with specific deadlines. This allows for better tracking of progress and maintaining motivation.

Importance of Flexibility

Financial circumstances can change, and goals need to be adjusted accordingly. It’s crucial to remain flexible and adapt your plan as needed. This may involve reassessing priorities or adjusting timelines.

Comparison of Financial Goal Types and Timelines

| Goal Type | Description | Timeline (Approximate) |

|---|---|---|

| Saving for a down payment on a house | Accumulating funds for a home purchase | 3-5 years or more |

| Paying off high-interest debt | Reducing or eliminating high-interest debts | 1-3 years or more |

| Building an emergency fund | Creating a safety net for unexpected expenses | 3-6 months of living expenses |

| Saving for a vacation | Accumulating funds for a trip | 1-2 years or more |

| Planning for retirement | Preparing for a secure retirement | 20+ years |

Developing a Joint Budget and Spending Plan

Financial health as a couple is significantly enhanced by a shared understanding and management of finances. A well-defined budget acts as a roadmap, ensuring both partners feel secure and empowered in their financial decisions. This shared financial plan is a cornerstone of a strong and thriving relationship.

Creating a Joint Budget

A joint budget is a detailed overview of all income and expenses, allowing for a comprehensive understanding of your financial situation as a couple. It’s a living document, not a static one, that should be reviewed and adjusted regularly to reflect changes in income, expenses, and financial goals.

Step-by-Step Guide to Creating a Joint Budget:

- Gather Information: Collect all relevant financial documents, including pay stubs, bank statements, bills, and receipts. This comprehensive data is crucial for an accurate assessment of your current financial position.

- Categorize Expenses: Divide expenses into categories like housing, utilities, groceries, transportation, entertainment, and debt repayment. This structured approach helps identify areas where you might be overspending or under-saving.

- Track Income: Record all sources of income for both partners, including salaries, side hustles, and any other financial contributions.

- Estimate Expenses: Accurately estimate monthly expenses for each category. Utilize past spending patterns as a guide, but be realistic and account for potential fluctuations. For example, utilities might fluctuate based on weather patterns.

- Compare and Discuss: Compare the gathered information and discuss any discrepancies or differences in understanding. Open communication is key to building a shared financial vision.

- Establish Realistic Goals: Identify shared financial goals, such as saving for a down payment on a house, paying off debt, or building an emergency fund. These goals provide motivation and direction for your budget.

- Review and Adjust: Regularly review your budget to ensure it aligns with your evolving financial situation and goals. Be prepared to adjust the budget as needed to accommodate changes in circumstances.

Transparency and Accountability

Transparency and accountability are vital components of a successful joint budget. Openly sharing financial information fosters trust and mutual respect, creating a supportive environment where both partners feel comfortable discussing financial matters. This promotes a healthy dynamic for financial decision-making.

Importance of Transparency:

- Building Trust: Transparency fosters trust and strengthens the relationship. Both partners feel secure knowing their financial contributions and needs are understood.

- Shared Responsibility: Accountability ensures that both partners feel responsible for contributing to the financial well-being of the household. This promotes a shared understanding of financial goals.

- Preventing Conflicts: Open communication and shared financial understanding reduce the likelihood of misunderstandings and conflicts.

Budgeting Tools and Resources

Numerous budgeting tools and resources are available to assist in creating and maintaining a joint budget. These tools range from simple spreadsheets to dedicated budgeting apps.

Examples of Budgeting Tools:

- Spreadsheet Software (Google Sheets, Microsoft Excel): Excellent for customized budgeting and tracking expenses.

- Budgeting Apps (Mint, Personal Capital): Provide user-friendly interfaces for tracking expenses, creating budgets, and visualizing spending patterns.

- Financial Advisors: Professionals who can provide personalized guidance and support for developing and managing a joint budget.

Managing Joint Expenses

Different approaches can be used to manage joint expenses. One method is to allocate a specific amount for each category, ensuring a clear division of responsibilities.

Approaches to Managing Joint Expenses:

- Joint Account: A single account for all shared expenses, allowing for easy tracking and splitting of costs.

- Individual Accounts: Each partner maintains a separate account for personal expenses, with designated funds for joint expenses.

- Splitting Expenses: Expenses are split based on pre-determined percentages or agreed-upon methods.

Allocating Funds

Allocation of funds should consider both shared needs and individual desires. For instance, shared needs could be housing, utilities, and groceries, while individual desires could include personal hobbies or savings for individual goals.

Tracking Joint Expenses and Income

A well-structured table helps track expenses and income effectively. The table should be easily accessible and adaptable to changes.

| Date | Description | Category | Amount | Paid By | Notes |

|---|---|---|---|---|---|

| 2024-08-27 | Rent Payment | Housing | $1500 | Both | Regular monthly payment |

| 2024-08-27 | Groceries | Groceries | $250 | Partner A | Weekly shopping |

| 2024-08-27 | Electricity Bill | Utilities | $100 | Both | Monthly bill |

Managing Debt and Financial Challenges

Taking on debt, whether individually or jointly, can significantly impact a relationship. Proactive management of debt is crucial for maintaining financial stability and preventing potential conflicts. Open communication and a shared plan are essential for navigating financial challenges effectively and strengthening the bond between partners.Addressing debt proactively is not just about paying it off; it’s about understanding the root causes, creating a sustainable strategy, and fostering a united front against financial strain.

This approach builds trust and encourages a collaborative atmosphere, making it easier to weather any financial storm.

Importance of Addressing Debt Proactively

Proactive debt management is essential to avoid escalating financial problems. Delayed action can lead to increased interest charges, impacting both the individual and joint financial well-being. A proactive approach fosters open communication, builds trust, and allows for early adjustments to spending habits. This allows for greater control over the financial future, preventing the feeling of being overwhelmed by debt.

For instance, addressing a small credit card debt early can prevent it from snowballing into a larger, more complex problem.

Strategies for Managing Joint Debt

Effective joint debt management relies on shared responsibility and open communication. This involves establishing clear agreements on who is responsible for which debts and how payments will be distributed. Joint accounts for shared debts can be beneficial, as long as both partners understand the associated responsibilities. Creating a shared budget, as discussed previously, will be invaluable in tracking expenses and making informed decisions about debt repayment.

Creating a Plan to Reduce Debt Together

A comprehensive debt reduction plan should include identifying all outstanding debts, evaluating interest rates, and prioritizing repayment based on high-interest debts. Using a debt snowball or avalanche method can provide a structured approach to debt reduction. For example, the debt snowball method prioritizes paying off the smallest debts first to build momentum and motivation. The debt avalanche method, on the other hand, prioritizes debts with the highest interest rates first to save money on interest over time.

Potential Conflicts and Disagreements Related to Debt Management

Disagreements regarding spending habits, priorities, or repayment strategies are common in shared debt situations. Differing opinions on financial decisions, like impulsive purchases or differing spending styles, can lead to conflicts. Addressing these issues head-on with respect and understanding is vital. For example, one partner might prefer a slow and steady approach to debt reduction, while the other might prefer a more aggressive strategy.

Methods for Resolving Financial Disagreements Constructively

Open and honest communication is key to resolving financial disagreements constructively. Active listening, empathy, and a willingness to compromise are essential components of conflict resolution. Using “I” statements to express feelings and concerns, without blaming, can facilitate constructive dialogue. Consider seeking professional financial advice if disagreements persist, as a third-party perspective can offer valuable insights and guidance.

Comparing Debt Reduction Strategies

| Strategy | Description | Advantages | Disadvantages |

|---|---|---|---|

| Debt Snowball | Prioritizes paying off the smallest debts first. | Motivational, builds confidence, quickly shows progress. | Doesn’t maximize interest savings, may not be the most efficient. |

| Debt Avalanche | Prioritizes debts with the highest interest rates first. | Maximizes interest savings, most efficient in the long run. | Less motivating initially, requires more discipline. |

| Debt Consolidation | Combining multiple debts into one loan with a lower interest rate. | Simplifies payments, potentially lowers monthly payments. | May require a good credit score, could increase overall debt if not managed carefully. |

Communicating About Savings and Investments

Saving and investing are crucial components of a healthy financial relationship. Open communication about these strategies ensures both partners are aligned on financial goals and feel comfortable contributing to the future. It’s not just about the money; it’s about building a shared vision for your financial future together.Understanding each other’s comfort levels with risk and investment styles is essential.

A shared understanding of financial objectives, whether it’s a down payment on a house, retirement planning, or funding a child’s education, allows for a coordinated approach to achieve those goals.

Importance of Discussing Saving and Investment Strategies

Open communication about savings and investment strategies is vital for aligning financial goals and fostering trust. Different investment approaches and risk tolerances can lead to conflicts if not discussed beforehand. Having a common understanding of financial goals and risk tolerance allows for a joint approach that benefits both partners.

Examples of Different Investment Options and Risk Tolerance Levels

Different investment options offer varying levels of potential returns and risk. Conservative investments like savings accounts and certificates of deposit (CDs) typically provide lower returns but have a low risk. Moderate investments, such as bonds or mutual funds, offer a balance of potential return and risk. Aggressive investments, such as stocks or real estate, have the potential for higher returns but also involve greater risk.

Risk tolerance is an individual factor, and couples need to discuss and understand each other’s risk tolerance before making any investment decisions.

Process of Making Joint Investment Decisions

Joint investment decisions should involve open communication and mutual agreement. Partners should thoroughly research different investment options and understand the associated risks and rewards. A well-informed decision-making process is crucial to minimize disagreements and ensure both partners feel comfortable with the choices. Consider using a shared financial planning tool to track investments, manage budgets, and monitor progress toward financial goals.

Value of Diversification and Long-Term Financial Planning

Diversification across various asset classes, such as stocks, bonds, and real estate, can help mitigate risk and potentially increase returns over the long term. Long-term financial planning, which considers future needs and goals, is essential for sustainable wealth accumulation. This involves considering factors like retirement planning, education funding, and major life events.

Potential Conflicts or Disagreements Related to Investment Decisions

Disagreements regarding investment decisions are possible. Different risk tolerances, investment styles, and timelines for achieving financial goals can lead to conflicts. Open communication and mutual understanding of each other’s perspectives are crucial for resolving these conflicts and maintaining a harmonious financial relationship. It’s important to approach these conversations with respect and a willingness to compromise.

Table Outlining Various Investment Options and Their Associated Risks

| Investment Option | Potential Return | Risk Level | Description |

|---|---|---|---|

| Savings Account | Low | Very Low | A low-risk account offered by banks that typically pays a small interest rate. |

| Certificates of Deposit (CDs) | Low to Moderate | Low | A time deposit with a fixed interest rate and maturity date. |

| Bonds | Moderate | Moderate | Debt securities issued by corporations or governments. |

| Mutual Funds | Moderate to High | Moderate | A professionally managed portfolio of stocks, bonds, or other assets. |

| Stocks | High | High | Ownership shares in a company, with potential for significant returns but also substantial risk. |

| Real Estate | High | High | Investment in property, often with both rental income and potential capital appreciation. |

Handling Financial Disagreements

Financial disagreements are a common, though often challenging, aspect of any partnership. These disagreements can arise from differing financial priorities, spending habits, or even differing views on saving and investment strategies. Addressing these conflicts head-on with open communication and constructive strategies is key to maintaining a healthy and stable financial relationship.Open and honest communication about finances is essential for navigating these disagreements.

It’s crucial to create a safe space for discussing concerns without resorting to blame or judgment. Focus on understanding each other’s perspectives and finding common ground.

Strategies for Resolving Conflicts Constructively

Effective conflict resolution involves active listening, empathy, and a commitment to finding solutions that benefit both partners. By approaching disagreements with a calm and respectful demeanor, couples can effectively navigate even the most challenging financial situations.

- Active Listening: Pay close attention to what your partner is saying, both verbally and nonverbally. Try to understand their perspective, even if you don’t agree with it. Avoid interrupting and focus on truly hearing their concerns.

- Empathy: Try to put yourself in your partner’s shoes and understand their feelings. Acknowledge their emotions and validate their concerns, even if you don’t fully agree with their perspective. Acknowledging their feelings is crucial for a productive discussion. A simple “I understand how frustrating this is” can go a long way.

- Healthy Communication Techniques: Employ “I” statements to express your feelings and needs without placing blame. Focus on describing the impact of the situation on you, rather than criticizing your partner. For example, instead of saying “You always spend too much,” try “I feel stressed when we don’t stick to the budget.” This shifts the focus from blame to understanding.

- Seeking Professional Advice: If disagreements persist despite your best efforts, consider seeking guidance from a financial advisor. A neutral third party can offer objective perspectives and help facilitate a constructive discussion. This is particularly helpful when emotions run high.

Examples of “I” Statements

Using “I” statements is a powerful tool in resolving disagreements. It helps to express feelings and needs without placing blame. By focusing on how a situation affects you, you create a more constructive dialogue.

| Situation | “I” Statement (Example) |

|---|---|

| Partner consistently overspending on entertainment. | “I feel anxious when our entertainment spending exceeds our budget. I’m concerned about the impact on our savings goals.” |

| Partner avoiding discussions about debt. | “I feel frustrated when we avoid talking about our debt. I need us to create a plan to address it.” |

| Disagreement on investment strategy. | “I’m concerned that our current investment strategy doesn’t align with our long-term financial goals. I’d like to discuss alternative options.” |

| Partner’s reluctance to save. | “I feel disappointed when we don’t save a significant portion of our income. I believe saving is important for our future.” |

Conflict Resolution Strategies

Effective conflict resolution is a vital aspect of any relationship, particularly when finances are involved. The key is to approach the discussion with a willingness to understand each other’s perspectives. By using specific strategies, couples can resolve conflicts peacefully and collaboratively.

- Compromise: Finding a solution that satisfies both partners’ needs as much as possible is key to long-term financial stability. Finding common ground is essential to building a strong foundation.

Maintaining Open Communication Over Time

Financial health, like any relationship, thrives on consistent communication. A shared financial future requires a commitment to ongoing dialogue, not just an initial conversation. Open communication isn’t a one-time event; it’s an ongoing process that adapts to life’s inevitable changes. This involves recognizing that your financial situations and goals may evolve, and being prepared to adjust your plans together.Maintaining open communication is essential for navigating the ups and downs of life, whether it’s a new job, a major purchase, or unexpected expenses.

It fosters trust, prevents misunderstandings, and allows you to proactively address any financial challenges as they arise. This continuous dialogue ensures your financial plan remains relevant and effective in achieving your shared goals.

Adapting Financial Plans to Life Changes

Regular check-ins about finances are crucial. Life events, both planned and unplanned, can impact your financial situation, requiring adjustments to your budget and spending plan. Proactive communication allows you to respond to these changes effectively.

- Recognizing and Responding to Life Events: Life events such as starting a family, purchasing a home, or experiencing job loss necessitate adjustments to your financial plan. Open communication ensures that you both understand the impact of these events and can collaborate on new strategies to maintain financial stability. For example, a couple expecting a child may need to re-evaluate their savings goals and adjust their spending plan to accommodate childcare expenses.

- Budget Adjustments: Adjusting the budget in response to life events requires careful consideration of increased or decreased income, expenses, and financial obligations. Regular reviews and modifications are crucial for maintaining financial equilibrium. For instance, a couple with increased income might allocate more to savings or debt repayment, or a couple facing a temporary loss of income might need to cut back on discretionary spending.

- Savings and Investment Strategies: Life events might necessitate shifts in your savings and investment strategies. For example, if one partner takes on a new role or career that requires higher education, adjusting investment goals to reflect the time horizon and desired returns is essential.

- Debt Management: Unexpected life events might necessitate re-evaluating debt management strategies. For example, a serious illness might impact the couple’s ability to make debt payments, necessitating a discussion about restructuring or renegotiating existing debt obligations.

Methods for Discussing Financial Changes

Effective communication is vital to navigating financial changes constructively.

- Scheduling Regular Financial Check-ins: Establish a regular schedule for discussing your finances, whether it’s weekly, monthly, or quarterly. This structured approach allows you to address changes proactively and avoid accumulating financial stress. For example, a monthly review of income, expenses, and savings can identify potential issues before they escalate.

- Using a Financial Calendar or Planner: Employ a financial calendar or planner to track income, expenses, and financial milestones. This visual tool can help you anticipate potential financial challenges and discuss solutions together. For example, a shared Google Sheet or online financial planner can be used for tracking and sharing financial data.

- Active Listening and Empathy: Active listening and empathy are crucial during financial discussions. Pay close attention to each other’s perspectives and feelings, showing genuine understanding and respect. For example, actively listening to concerns and empathizing with each other’s financial pressures can foster a more constructive dialogue.

- Seeking Professional Advice: When facing complex financial situations, consider seeking advice from a financial advisor. This can provide objective guidance and support in navigating challenging financial decisions. For example, a financial advisor can help develop a comprehensive financial plan that takes into account various life events.

Ongoing Financial Education

Continuous learning is key to maintaining a strong financial foundation.

- Learning Together: Actively participate in financial education together, whether through workshops, seminars, or books. This shared learning experience fosters a deeper understanding of financial concepts and strengthens your ability to navigate financial challenges. For example, attending a workshop on budgeting or investment strategies can help you both develop better financial literacy.

- Staying Updated on Financial Trends: Stay informed about current financial trends and economic conditions. This knowledge enables you to make informed decisions about your finances. For example, understanding inflation or interest rate changes can help you adapt your financial plan accordingly.

Closure

In conclusion, successfully navigating financial discussions with your partner requires proactive communication, empathy, and a commitment to understanding each other’s needs and perspectives. By following the steps Artikeld in this guide, you can foster a healthy financial partnership, build trust, and create a solid foundation for your future together. Remember, open communication and proactive planning are key to long-term financial success within your relationship.